There has been speculation for some time about what would happen if Saudi Arabian oil installations were knocked out.

Equally so about how US President Donald Trump would act if he became sucked into a potential military crisis.

What would it mean for oil prices, tanker rates and global economic growth — never mind geopolitics and prospects of war? Well this scenario is now in play.

'Biggest thing'

As a top London tanker broker told me on Monday: “This is the biggest thing that I have ever had to deal with.”

And what happens in these nervous days ahead is just the start. This is an event that will rattle the collective cage for a long time to come.

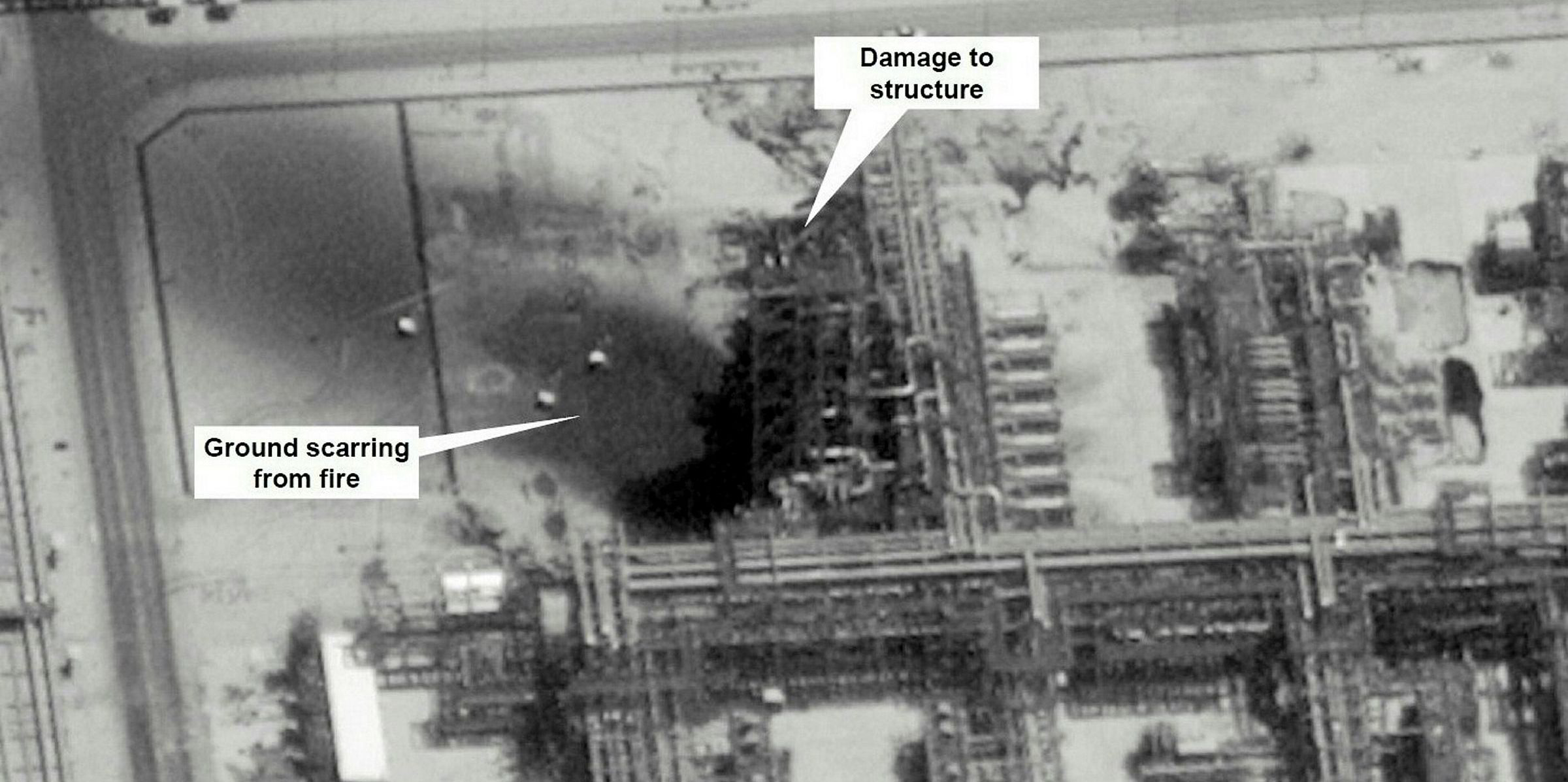

Saudi Arabia is the world’s biggest oil exporter and it has proved itself to be highly vulnerable to a sudden and devastating attack. Whether it was carried out by Tehran-backed Houthi rebels or Iran itself is partially irrelevant.

You can disrupt Saudi Arabia or the wider oil-dependent Western economies seemingly with readily-available drone technology.

Half of the desert kingdom’s production has been taken out of commission in one fell swoop: 5.7m barrels per day (bpd). Abqaiq is the world’s largest oil processing plant and lies at the heart of the country’s hydrocarbon infrastructure.

There is plenty of oil in storage in the kingdom — around 185m barrels in total — that can, in the short term, mitigate the situation. But the longer it is out of action, the worse it will be.

There is plenty of oil in storage in Saudi Arabia — around 185m barrels in total — that can, in the short term, mitigate the situation. But the longer it is out of action, the worse it will be

The oil markets reflected the scale of this drama appropriately. Crude prices rocketed 20% to $72 per barrel in the immediate aftermath of last Saturday’s attack, their biggest intraday rise in more than 30 years.

Surge in tanker rates

Tanker rates surged too. If you wanted to charter VLCCs out of the Middle East Gulf eastwards, it would cost at least 30% more.

Product tankers have also seen better rates as buyers seek alternative fuel supplies from places such as the Far East, where there is a current oversupply.

Meanwhile, US experts are poring over the debris to find confirmation as to who exactly is responsible for the attack.

Trump has declared the US is “locked and loaded” for its own missile strikes on Iran, if strong evidence points to Tehran.

Military action in the region — long mooted since Trump reintroduced sanctions on Iran — would only disrupt wider oil movements from the region.

But despite the bellicose Twitter feed and his seemingly volatile nature, Trump has held back from military action so far.

He sacked his pugnacious security advisor John Bolton last week and, in recent days, said he would “like to avoid” war with Iran.

Trump has also acted pragmatically to ease oil supplies by announcing the opening of the country’s Strategic Petroleum Reserve.

We don't know what China — currently the world’s biggest oil importer and key recipient of Saudi crude — will do, but it too has a strategic reserve with more than a month’s worth of crude in it.

The pre-weekend oil price had factored in US/China trade wars, Brexit and general concerns about the global economy.

But there was no real premium for geopolitical risk. There is now.

Bad situation

The whole event is bad for tankers and bad for bunker prices — and bad for the world economy and consumer confidence.

Carnival Corp shares fell 3% at the start of this week on the back of just these wider worries. The company’s capital value is more than a quarter less than 12 months ago.

In the meantime, there are gains to be made by tanker operators as crude and product supply patterns switch away from the Middle East Gulf to West Africa, South America and the US itself.

Some tanker stocks, such as Frontline, soared in the immediate aftermath of the Saudi attacks only to sink as the week developed.

Clarksons Platou Securities has estimated a potential 2.5m bpd reduction in overall seaborne trade to 40m bpd — and that is with other Opec countries plus the US increasing its output.

The big oil importers, such as China and India, can only suffer at a sensitive time for global economic growth.

The Saudi attack is not an “unprecedented disaster”, to quote one US financial broker, but it is certainly a hugely significant event.