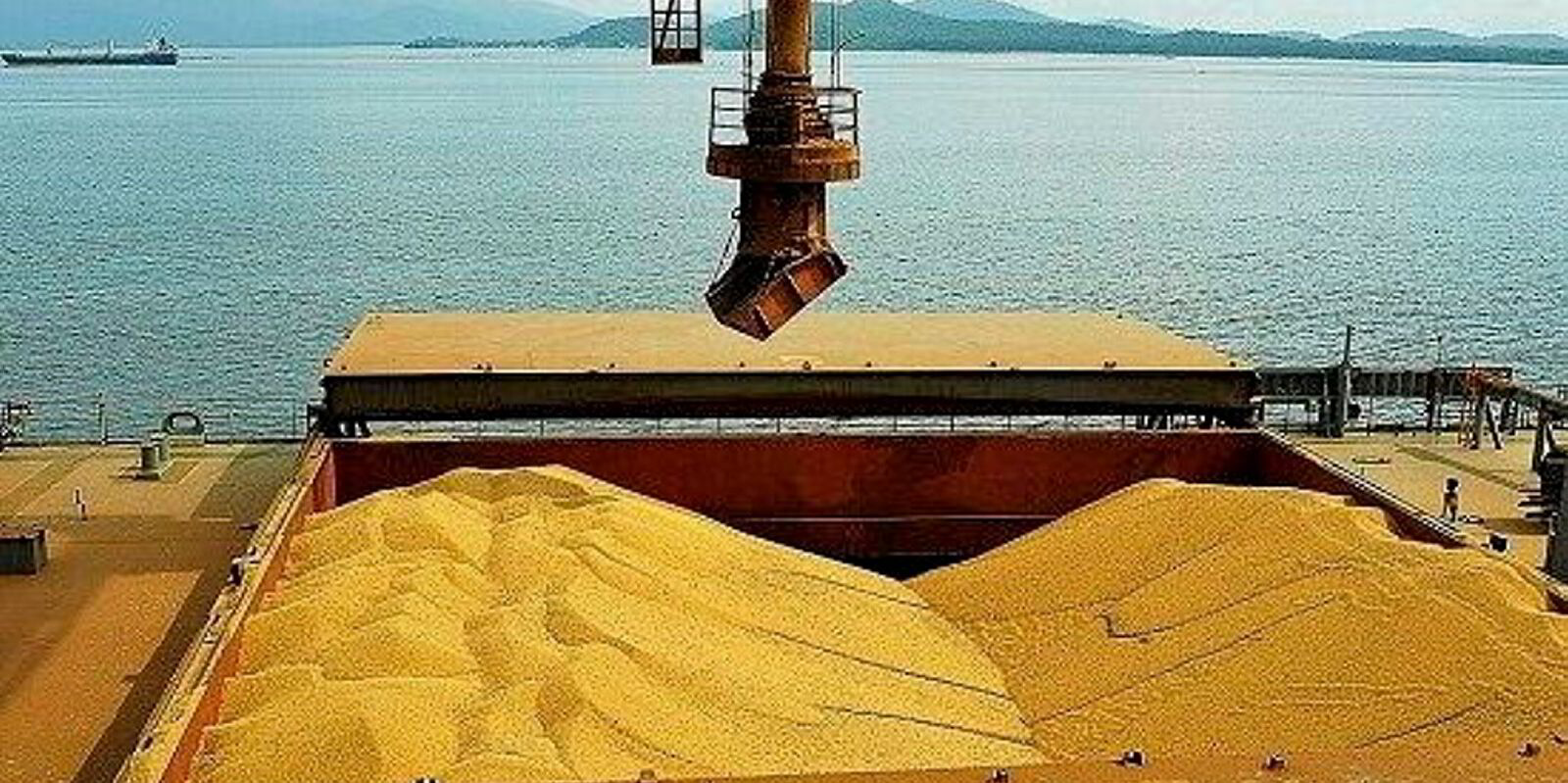

China’s reluctance to buy US soy in favour of South America is set to continue into the third quarter of 2024, as the importer fears an unfavourable US trade policy.

Kpler lead agricultural commodities analyst Ishan Bhanu told TradeWinds: “The main concern for freight will be lower soybean exports out of the US.

“This is because, like in 2019, China may decide to severely limit imports from the US. And it is already showing signs of doing that.”

The P7 panamax route on the Baltic Exchange, from the Mississippi River to the Chinese port of Qingdao, China, was last at $57.257 per tonne, down from its 2024 peak of $65.576 per tonne seen in March.

“China is buying less from the US because they expect an unfavourable trade policy and a possible trade war if Donald Trump gets elected as president,” Bhanu said.

“In case of a Democratic win, some of this concern should subside, but we’ll only know that in December. Until then, we’re estimating lower soybeans from the US to China.”

In this scenario, Kpler expects US soy exports to China to slip to 19.13m tonnes in the 2024-25 season, down from 24.7m tonnes in 2023-24 and 31.5m tonnes in 2022-23.

Kpler also indicated that, although congestion at Chinese ports is less likely than it has been in the past, this development is still one to watch.

“As China is aggressively importing Brazilian soy right now, to avoid buying US product later this year, this could potentially lead to congestion when all these vessels arrive in August/September,” Bhanu added.

China’s seaborne soybean imports were just over 101m tonnes in 2023, according to Clarksons. Volumes are forecast at 101m tonnes in 2024 and 105m tonnes next year.

US sailing distances shorten

China’s diversification in its imports of grains — such as soy, corn and wheat — away from the US has been a notable trend over the past three years, Bimco also noted in its latest report.

The US accounted for 37% of grain shipments to China in 2021. However, last year the share declined to 23%. Competition from Brazil and Argentina, which often export at lower prices, has been a factor, as well as China also lifting restrictions on corn shipments from Brazil in 2022 and from Argentina in May this year.

However, the US is expected to see a ramp-up in its corn and soy exports during 2024, albeit more “locally”, as water in the Mississippi River is at more normal levels, facilitating the transport of its harvests to seaports.

Bimco shipping analyst Filipe Gouveia said: “A recovery in corn shipments from the US would boost the global grain supply, supporting bulk carriers in the panamax, supramax and handysize segments.

“However, gains from dry bulk demand could be limited. Under regular conditions in the Panama Canal, sailing distances to importing markets in Asia are shorter from the US than from Brazil and Argentina.”

Between January and July, sailing distances for US grain shipments stagnated due to a change in destinations, it indicated. The US has boosted its grain shipments to countries closer to its shores, such as Mexico and Colombia, while its shipments to China have fallen 19% year on year.

However, the disruptions in the Panama Canal were still positive for sailing distances of US grains, as several ships were rerouted around the Cape of Good Hope, it said.

Consequently, sailing distances for shipments to East Asia, which typically use the Panama Canal, increased 5% year on year. Gains would have been greater if some cargoes had not been rerouted overland to ports on the West Coast, Bimco added.

“So far in 2024, transit restrictions in the Panama Canal have gradually eased and are expected to have recovered ahead of the peak export season,” Gouveia said.

“A return to normal conditions would shorten sailing distances for US grain shipments, limiting gains from stronger volume. However, should shipments to Asia recover, this impact may be limited.”