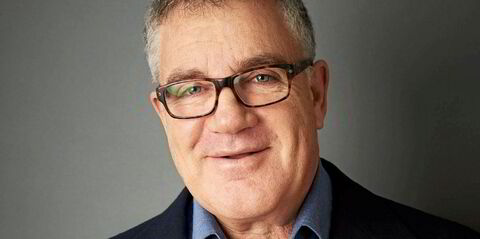

If you want to get Scorpio Tankers president Robert Bugbee going, ask whether his company should be handing out extraordinary or “special” dividends, or even high-payout regular ones.

He is not having it, at least as long as Scorpio continues to trade at a significant discount to its net asset value.

Bugbee and Scorpio chief executive Emanuele Lauro are fans of stock buybacks in that mode and have been quite clear in communicating that strategy to shareholders now that the owner has paid down its debt to below the scrap value of the fleet.

Bugbee explained why that is Scorpio’s priority in capital allocation in an interview with TradeWinds.

“If you have a reasonable discount to your NAV, then acquiring stock is the much better use of capital when compared with buying secondhand vessels or newbuildings, for starters,” Bugbee said.

“And it’s better than dividends. There’s no point in paying out loads of big dividends that aren’t sustainable. You’re just at some point going to have buyers of that stock that come a cropper [suffer a setback]. Once asset values stop going up, and earnings stop going up, ships do depreciate.”

Before we go further down that path, it is worth noting that this is a high-class problem for Scorpio to have.

Struck by the Covid-19 clampdowns of 2020, Scorpio was in a bad place, placing nearly its entire fleet of more than 100 product tankers under costly sale-leaseback financing that continued into 2021.

One or two analysts even raised questions about the owner’s ability to survive.

“It wasn’t worrisome, it was terrifying,” Bugbee said. “There were no cars on the road, no planes in the sky, and our debt interest payments were increasing every day.”

But with a rebound in tanker markets, Scorpio is now in Bugbee’s own words living the dream.

Record cash flows have allowed Scorpio to reduce total debt in May to $1.37bn from $3.2bn at the end of 2021. Net debt has plunged to $811m from $2.9bn.

These are heady times for shipowners across multiple sectors, including the public ones.

Years into a boom cycle, rampaging cash flows have allowed owners to make early repayments on bank debt, taking leverage levels to or near record lows.

That may not be good for the lenders, but it is a great place to be for the owners.

Still, it creates a new issue for the cash-rich owners: How to deploy all that capital, including pressure to return it to shareholders.

With the annual Marine Money Week looming in New York, TradeWinds’ finance business report takes a look at how the three major Manhattan-based owners — International Seaways, Genco Shipping & Trading and Scorpio Tankers — are approaching the challenge of capital allocation.

(There is an asterisk next to Scorpio: the owner is technically based in Monaco, but its large New York office houses the president, chief financial officer and chief operating officer).

Scorpio favours share buybacks, while Genco and chief executive John Wobensmith preach the virtues of robust dividend payouts.

Seaways, meanwhile, offers a balanced approach that some might find boring, but which management says will carry the day in the long term.

The net debt figure is roughly what Bugbee cited last November when he said on an earnings call that Scorpio would shift priority from debt reduction to capital returns once borrowing fell below the fleet’s scrap value.

On 20 March, Bugbee said in an interview with TradeWinds that the goal looked reachable in the second quarter, adding, “we’re certainly not going to a defined high-dividend payout policy” while ruling out extraordinary dividends.

The statement felt like a shot across the bow of hedge funds and certain other investors who might be agitating for big dividends. Then Scorpio formalised the policy in reporting first-quarter earnings.

Scorpio did in February increase its regular dividend to $0.40 per share from $0.35, which represents about a 2% yield on the current trading price near $80 per share.

“We believe strongly in sustainable regular dividends — something that can be relied upon,” Bugbee said in an interview for this article.

“Extraordinary dividends by definition cannot be relied on. They don’t commit the company to anything. But the shareholders start to rely on it and if it’s not paid one day, then there’s something wrong.

“The full-payout regular dividends are tremendously exciting to the shareholders in the present. But they’re more attractive in certain tax regimes like Scandinavia that are not subject to the same dividend taxes found in the US,” Bugbee said.

“It’s why some shareholders here prefer that the company keep that money, the stock goes up and they can sell in a year or whatever time under a better tax treatment.”

Still, he says it is about more than getting deep in the weeds of various tax protocols.

“It’s more philosophical than that. The high payouts prove to be unsustainable in our industry. And we can also point to the drilling industry or master limited partnerships to show that’s the case. Very often when the party is over, companies go bankrupt,” Bugbee said.

He said he is unable to calculate whether the majority of Scorpio shareholders support management’s approach, but he is confident there is strong backing.

“I’m convinced we have the support of our shareholder base for this policy,” Bugbee said. “The fact remains that a company that generates strong cash flows should retain its profit by lowering debt, increasing cash and buying back its own stock. The stock will go up.”

Scorpio’s stock has. It is up 27% so far in 2024, and 48% since the start of 2023. But the number is more like 500% since those dark days that held sway even at the start of 2022.

It does beg the question though. Even if Bugbee is right about the effectiveness of stock buybacks — and Scorpio is wielding a full $250m repurchase authorisation — what happens if and when the gap to NAV closes or flips to a premium?

That is a hypothetical he was not willing to address in this interview, although Bugbee added the following: “How much is too much cash? We’ve been very focused on getting to the debt levels we wanted to achieve. I have looked at some historical data. I haven’t found a public company in history that’s had too much cash.”