It has been quite some time since Scorpio Group president Robert Bugbee and equity analyst Amit Mehrotra got into what might be politely called a spirited disagreement over the shipowner’s management practices in a public forum.

So, Scorpio Bulkers' earnings call this week was one for nostalgia fans as the executive and the Deutsche Bank man went head to head over the outfit's share strategy.

At issue was New York-listed Scorpio Bulkers $100m investment last autumn in public sister company Scorpio Tankers, which had grown to a value of some $152.3m at Monday’s closing price of $28.12, with a further $500,000 in dividends paid.

$100m lifeline

While the related-party lifeline drew smirks from analysts at the time on governance and other grounds, it clearly has been a winner. Even Mehrotra referred to it as “a home run” on Monday’s call.

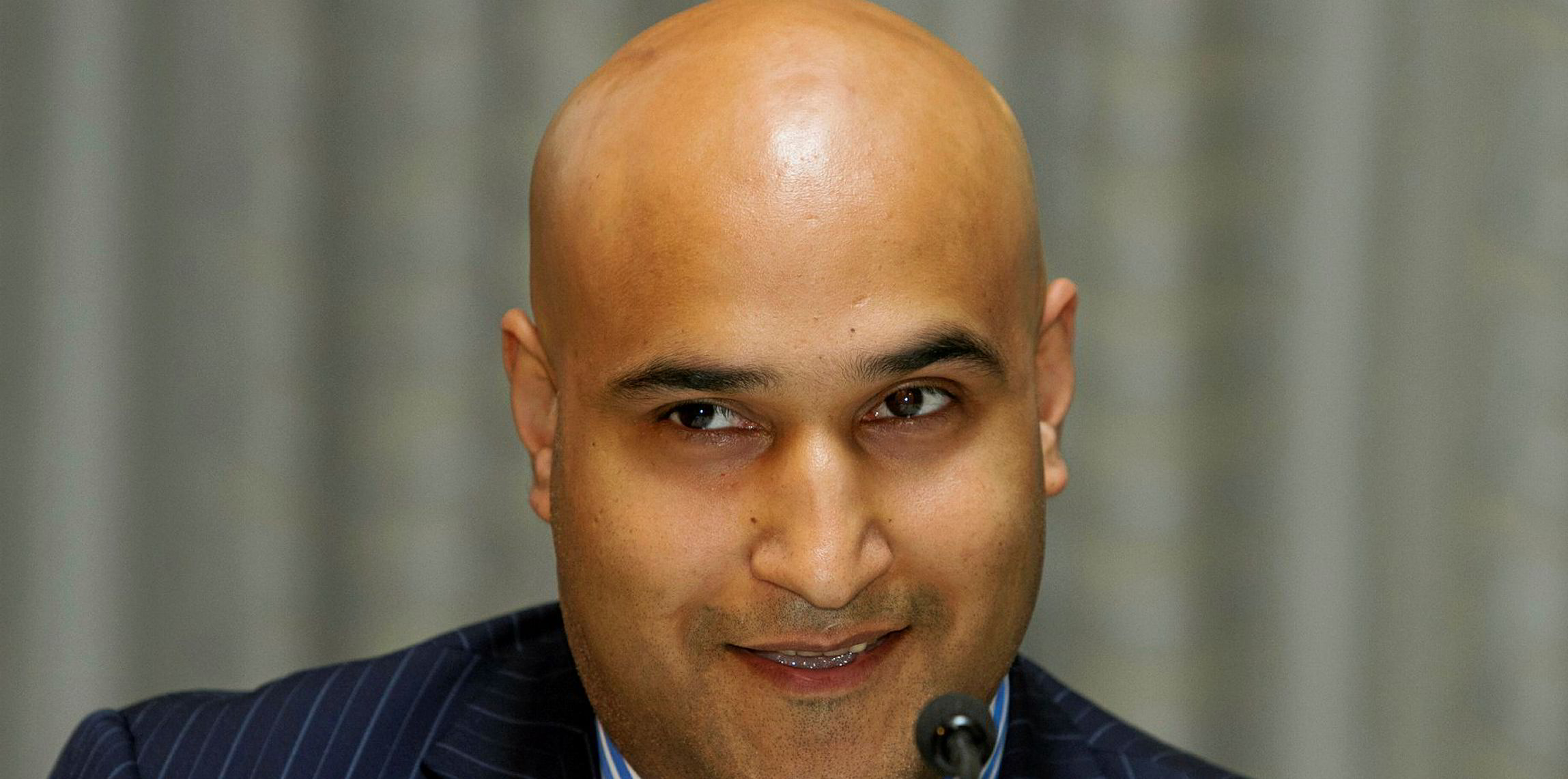

So what is the problem? As Mehrotra sees it, the investment to date has not done much to help out Scorpio Bulkers' shareholders.

“[The] increase in STNG has not corresponded to any real material increase in SALT’s equity value,” Mehrotra said, using the ticker symbols for Scorpio Tankers and Scorpio Bulkers, respectively.

[The] increase in STNG [Scorpio Tankers] has not corresponded to any real material increase in SALT’ [Scorpio Bulkers]'s equity value. You haven’t bought back one share of SALT [stock] [over the past quarter]

Amit Mehrotra

“You haven’t bought back one share of SALT [stock]” over the past quarter, Mehrotra protested.

The analyst’s point is this. While Scorpio Tankers has logged a massive gain, it is a paper profit — no shares have actually been redeemed. Scorpio Bulkers retains every share it bought in October at $18.50 each.

Share sale

Had it sold some shares and taken some of its winnings off the table, it would be in a position to use the proceeds to support Scorpio Bulkers shares, which trade at a massive discount to net asset value (NAV).

Bugbee himself suggested that the owner’s recent NAV has been about $10 per share. It closed Monday at $6.69 — about a 33% discount.

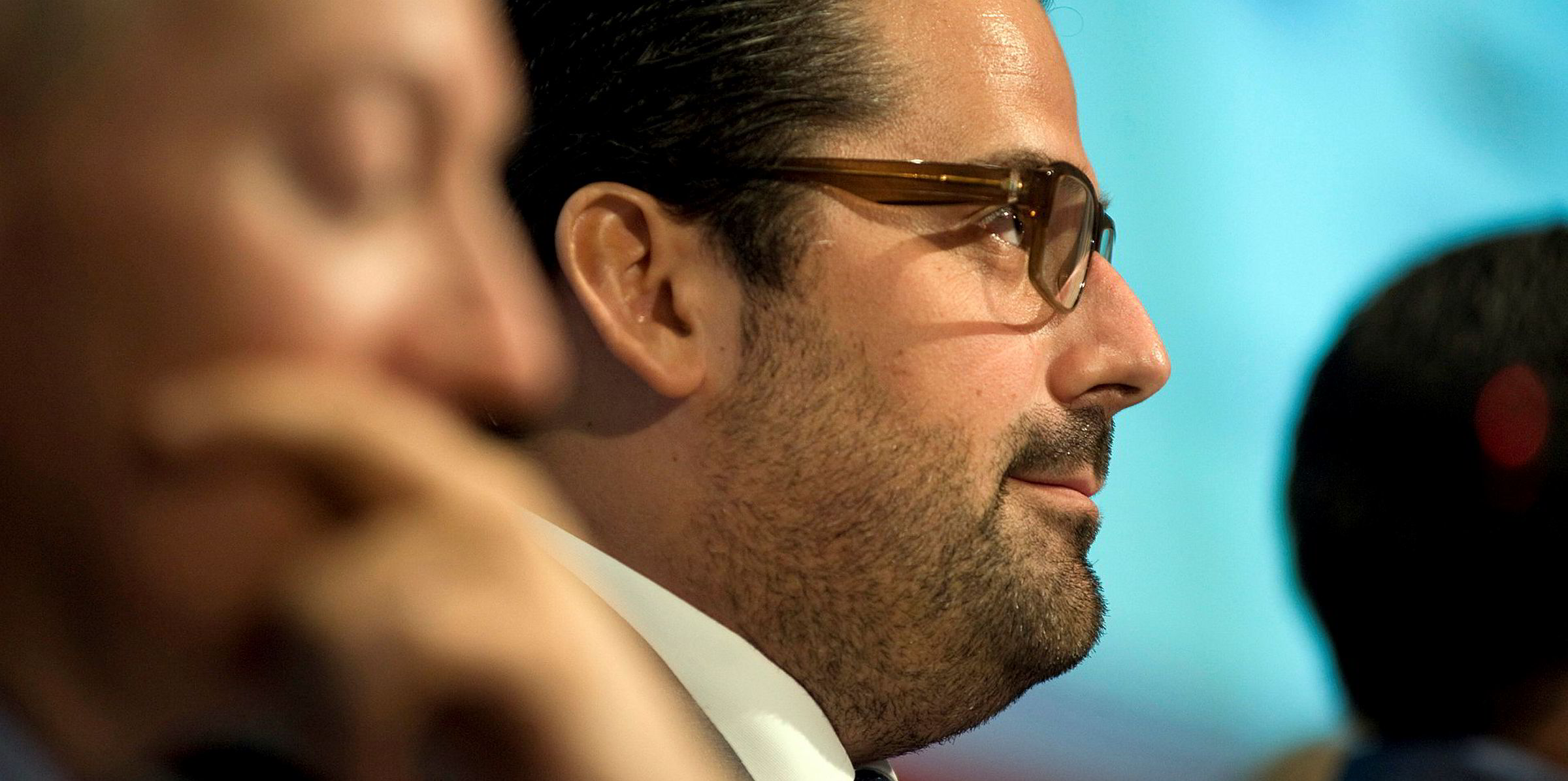

Yet so firm was Bugbee in management’s defence that he was moved to follow Mehrotra into his “home run” analogy, although he conceded it might be a mistake for an Englishman to discuss baseball.

“You said that STNG is a home run. I would say STNG's not quite a home run yet,” he said.

“I would say that STNG is on base. All we've done is hit a single and we got to first, and maybe we're starting — maybe we're crossing to second right now.”

In other words, while Scorpio Tankers has been on a roll in bolstering its share price, Bugbee suspects it is just getting started, especially with the effects of the IMO 2020 emissions regime just around the corner.

“STNG is better placed than, I think, virtually any other company there is in the world to benefit from that. And I think that it's important to — well, I think it's important to run that one out,” Bugbee said.

Large-scale purchase

With the world’s largest public fleet of products tankers at 109 units under ownership control, nearly all to be equipped with exhaust-gas scrubbers, Scorpio at least theoretically stands to see a double benefit: better hire rates caused by market dislocation, and lower fuel costs through its continued ability to burn high-sulphur bunkers.

But for Bugbee, the problem is not just selling Scorpio Tankers shares prematurely. It is also that Scorpio Bulkers shares would not remain such a bargain to buy under any large-scale purchase programme.

We would argue, with high conviction, that SALT’s management team has done little with respect to proactive value creation

Amit Mehrotra

Bugbee told Mehrotra that his own move to buy 125,000 Scorpio Bulkers shares in early July caused the stock price to rise by $0.20 over two days.

“You cannot go and sell $160m of STNG and go and buy $160m of stock in SALT at $6.0, $6.10 or at $4.58,” the last figure representing the average price Bugbee paid.

Mehrotra reluctantly moved on to other topics during the earnings call, but it was clear from an exchange with TradeWinds that he remained unconvinced by Bugbee’s rationale.

“The company will say that they can’t buy back much stock without driving the stock up ... but isn’t that the point?” he said.

“Shares are so dramatically below NAV that even if there is some technical impact it is still value accretive.”

The analyst also argued that Scorpio Bulkers shares are up only 19% on the year — the lowest among their dry bulk peers.

Creating value

“But the point we’re trying to get across is there is a fundamental difference between creating equity value and just having a stock go up in value,” Mehrotra said.

“We would argue, with high conviction, that SALT’s management team has done little with respect to proactive value creation this year despite what we view to be significant opportunity to do so.”

Bugbee said the numbers do the talking.

“SALT is up 20% year to date and STNG is up 50%. That is not an argument, that’s a fact,” Bugbee told TradeWinds.