Protection and indemnity clubs will struggle to justify increases in annual premiums at next February’s renewal after two years of profits and low claims, says insurance broker Aon.

Most of the 12 members of the International Group of P&I Clubs are in robust financial shape.

Many of them have reported combined ratios of below 100% for two years, indicating underwriting profits, the broker said in its July bulletin.

Despite strong underwriting performance, increases at renewal ranged from 5% to 7.5% in February this year owing to previous poor investment results that hit clubs’ reserves and concerns over inflation-based cost rises.

Latest figures show that investment results rebounded last year. Claims have also continued at low levels for several years.

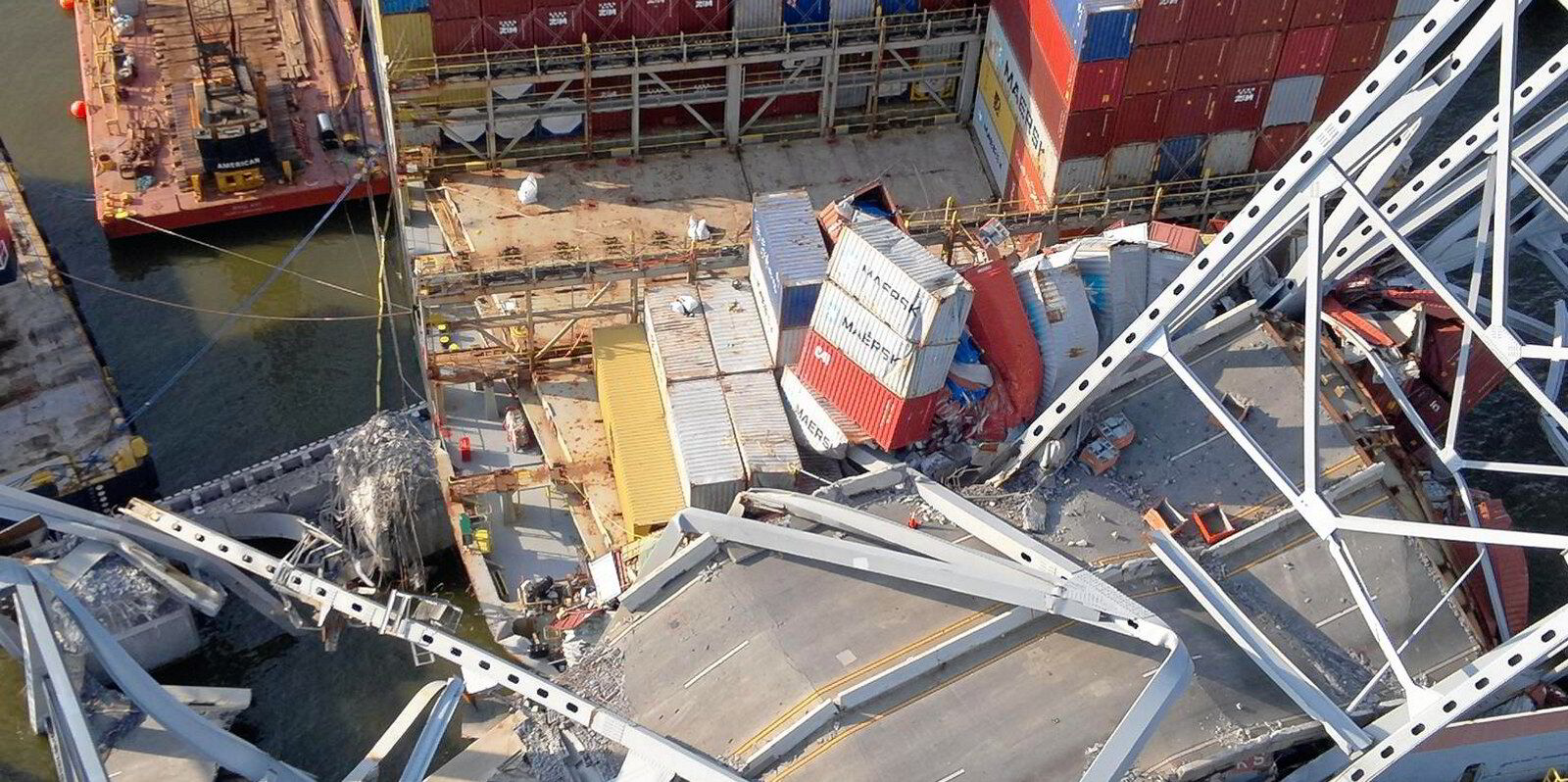

The claims have been moderate so far in 2024, despite the looming largest-ever maritime insurance case after the 9,962-teu container ship Dali (built 2015) struck and brought down a bridge in Baltimore, Maryland in March, killing six construction workers.

However, that is likely to have only limited financial impact on Britannia P&I, the provider for the Dali, and the rest of the pool as reinsurers will take the strain, said Aon.

“With this backdrop, it will be very difficult for clubs to justify increases again at the 20 February 2025 renewal,” it added.

“Most clubs are still prepared to quote extremely cheaply for new tonnage, which undermines overall underwriting performance and drives the need for increases at renewal.”

Aon’s stance follows similar comments from Mark Cracknell, head of P&I at broker Marsh, who told TradeWinds that increases were not justified in 2025.

The Aon bulletin also highlighted what it said was a widening gap between the biggest clubs and the less financially secure ones.

It highlighted reductions in tonnage for the American Club, Swedish Club and Japan Club, among the smallest of the P&I mutuals.

Some of the smaller clubs have also made unbudgeted additional calls on their members to bolster their finances in recent years, but the stronger recent results make that less likely for now, according to Aon.

“This gap between the well-performing clubs and those not doing so well is widening and becoming a common theme,” the report said.

“For a few of the clubs it would only take one or two bad years for unbudgeted supplementary calls to be required.

“This, alongside the fact that the larger, financially stronger clubs are returning premium to their members, is undoubtedly contributing to the widening of the gap between the clubs.”

The 12 members of the International Group supply P&I cover for 87% of the oceangoing fleet.

But the merger of two clubs to form NorthStandard in February last year sparked debate about potential further tie-ups and the long-term prospects of the clubs.

Strong financial results in 2023 dampened speculation. Some clubs insist they see a rosy future for smaller clubs providing specialist services to shipowner members.

Aon said it supports the diversification of clubs outside of purely mutual P&I business, with market frontrunner Gard leading the way.

Aon said the picture was not so simple this year, with the benefits of providing hull and machinery cover less clear.

It highlighted excellent results from Gard and Skuld, which have diversification as part of their strategy, and Steamship, which does not.

Read more

- Aon calls for passenger ship insurance review 11 years after the Costa Concordia

- Aon warns shipowners over ‘thermonuclear’ personal injury awards

- Broker Aon spots trend toward ‘financially stronger’ P&I clubs

- Insurance broker Miller expands in Asia with new hire

- Shipowners should benefit from a ‘remarkable’ year of low pool claims, says broker Aon