Star Bulk Carriers’ roughly $500m acquisition of Connecticut-based Eagle Bulk Shipping this week is the capstone — for now — on nearly a decade of consolidation moves and its largest acquisition since 2014.

This week’s play on New York-listed Eagle’s fleet of 52 supramax and ultramax bulkers is the 10th time Star has moved on targets ranging from a few ships to an entire fleet or company, using its stock to backstop the acquisition in each case.

But to find a takeover the size of this week’s deal with Eagle, one has to look back to 2014, when the Greek owner moved on both principal Petros Pappas’ private Oceanbulk fleet and then US-listed Excel Maritime within two months.

Star’s buy of the 34-strong Excel fleet formerly led by Gabriel “Villy” Panayotides for $635m in cash and shares in August 2014 came weeks after its shares-based acquisition of 41 bulkers from Oceanbulk — a private venture between Star principal Petros Pappas and financier Oaktree Capital Management.

Those were the biggest pieces of Star’s growth before this week, but there has been a spate of smaller deals from 2018 on.

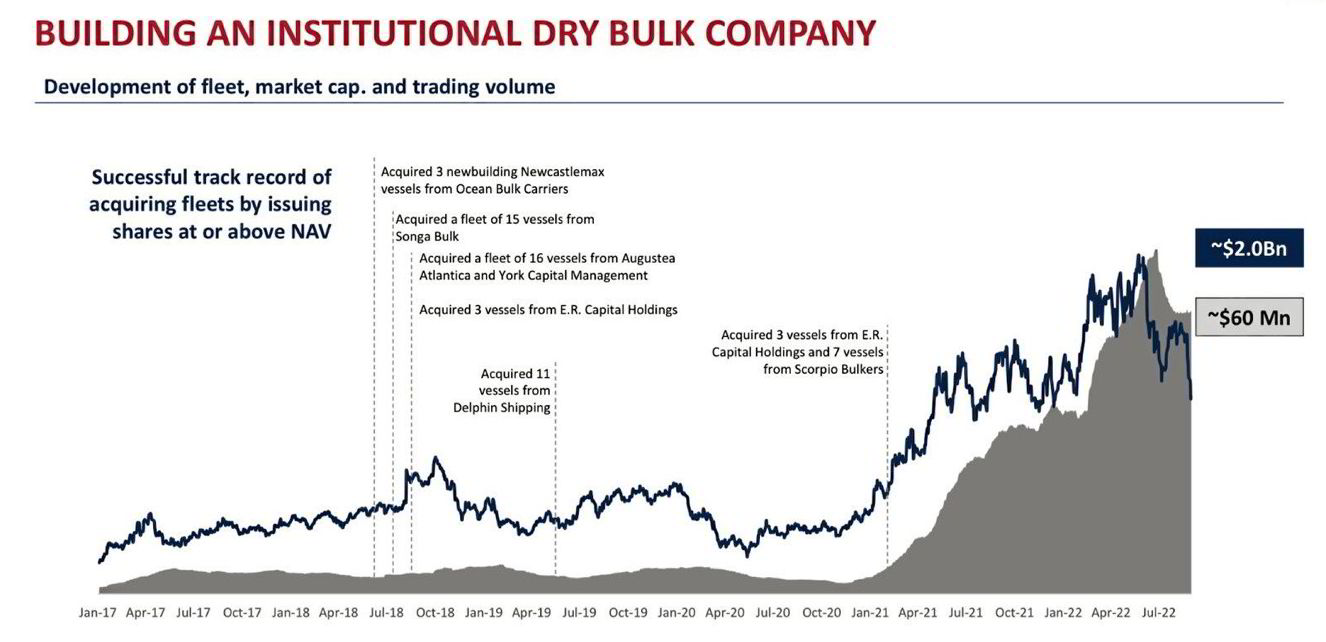

As TradeWinds reported in February 2022, Star had at that time acquired about half of its vessel count over the previous three years by snatching up a series of fleets.

It struck successive deals with Songa Bulk, Augustea Atlantica, ER Capital, Delphin Shipping and Scorpio Bulkers, each time acquiring either a full fleet or, in Scorpio’s case, a seven-vessel chunk.

Each time, Star has used a blend of its own shares alongside cash as payment, with Songa Bulk’s Arne Blystad and Augustea’s Italian Raffaele Zagari joining the Star board.

“The sellers wanted to take our shares,” Star president Hamish Norton said at the time. “To do a deal like that, you need to have a share that people want.”

While the timing on some of the deals might have aged better than others, that’s somewhat beside the point: Star’s goal is scale, as its executives have made clear on more than one occasion.

For example, Norton told a finance conference in 2022 that the average size of a company within the Russell 2000 — the benchmark index of US-listed “small cap” stocks — is $3.8bn.

“There aren’t too many shipping companies that are worth $3.8bn,” Norton said. “There aren’t too many shipping companies that are at $3.8bn at the top of the cycle, let alone at the bottom.

Mid-cap ambition

“That’s our ambition when we grow up. We want to be solidly mid-cap at the bottom of the cycle.”

Norton’s point about the top and bottom of cycles is also instructive. At the time, the dry bulk market was nearing a peak, and Star boasted a market capitalisation of nearly $2.6bn.

When the deal was announced on Monday, Star’s overall share value was closer to $1.8bn, with the Eagle acquisition tipped to boost pro forma market cap to $2.1bn.

Star has not gotten smaller, but the dry bulk market has weakened.

Pappas reiterated on an investor call following Monday’s announcement that Star is not done growing. It just needs some time to digest the Eagle deal.

“This is a merger with a supramax company, but we don’t rule out mergers with companies that run bigger vessels in the future,” he told equity analysts.